VANCOUVER, British Columbia, (GLOBE NEWSWIRE) — MGX Minerals Inc.(“MGX” or the “Company”) (CSE: XMG / FKT: 1MG / OTCQB: MGXMF) is pleased to announce the engagement of Quantec Geoscience (“Quantec”) to complete a Time Domain Electromagnetic (TDEM) survey on the Salinitas lithium brine project (the “Project”) in the Salinas Grande Salar of northwest Argentina. MGX has partnered with A.I.S. Resources (AIS.V) on the Project and is currently earning an 80% interest. The TDEM geophysical survey will be conducted along 52 stations spaced in 500 meter intervals across the edge of the salar to test for shallow, near surface brines to determine locations with anomalous concentrations of lithium.

About the Salinitas Lithium Brine Project

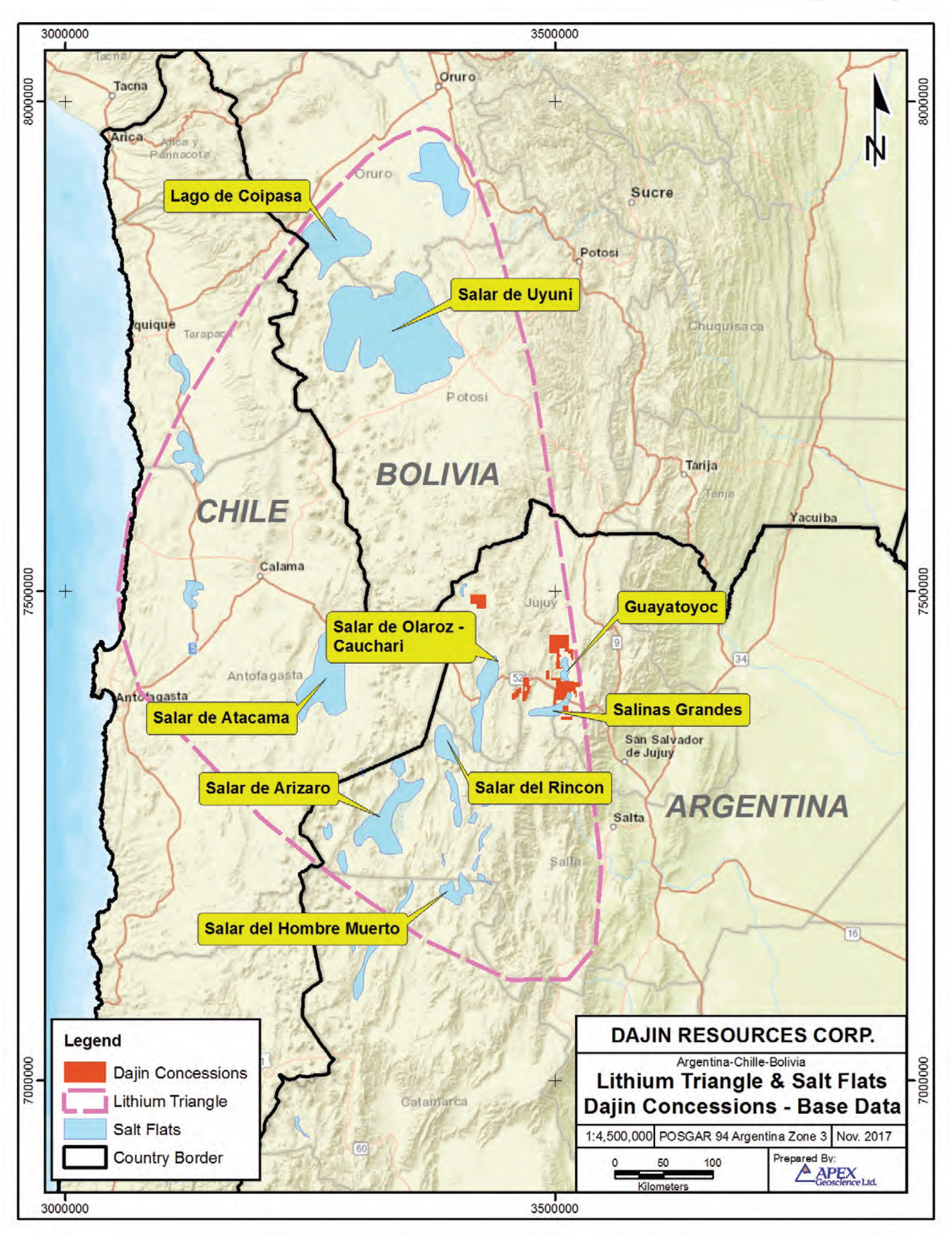

The Salinitas tenements are located in the lithium triangle of Argentina, Salar de Salinas Grandes, Province of Salta. The 4,308 hectare contiguous land package resides in the Puna region of northwest Argentina near the border of Chile, an area renowned for its lithium- and potassium-rich brine resources. MGX can earn an undivided 80% interest at any time during the Agreement by making payments totaling US$3.2 million. MGX has also agreed to incur total expenditures of at least US$1.2 million prior to May 31, 2020.

Rapid Lithium Brine Extraction Technology

MGX has developed a rapid lithium extraction technology eliminating or greatly reducing the physical footprint and investment in large, multi-phase, lake sized, lined evaporation ponds, as well as enhancing the quality of extraction and recovery across a complex range of brines as compared with traditional solar evaporation. This technology is applicable to petrolithium (oil and gas wastewater), natural brine, and other brine sources such as lithium-rich mine and industrial plant wastewater. The technology was recently chosen as winner of the Base and Specialty Metals Industry Leadership Award at the 2018 S&P Global Platts Global Metals Awards, held in London in May (see press release dated May 18, 2018).

Qualified Person

Andris Kikauka (P. Geo.), Vice President of Exploration for MGX Minerals, has prepared, reviewed and approved the scientific and technical information in this press release. Mr. Kikauka is a non-independent Qualified Person within the meaning of National Instrument 43-101 Standards.

About MGX Minerals

MGX Minerals is a diversified Canadian resource company with interests in advanced material and energy assets throughout North America. Learn more at www.mgxminerals.com.

Neither the Canadian Securities Exchange nor its Regulation Services Provider (as that term is defined in the policies of the Canadian Securities Exchange) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements This press release contains forward-looking information or forward-looking statements (collectively “forward-looking information”) within the meaning of applicable securities laws. Forward-looking information is typically identified by words such as: “believe”, “expect”, “anticipate”, “intend”, “estimate”, “potentially” and similar expressions, or are those, which, by their nature, refer to future events. The Company cautions investors that any forward-looking information provided by the Company is not a guarantee of future results or performance, and that actual results may differ materially from those in forward-looking information as a result of various factors. The reader is referred to the Company’s public filings for a more complete discussion of such risk factors and their potential effects which may be accessed through the Company’s profile on SEDAR at www.sedar.com.

https://aisresources.com/wp-content/uploads/2016/11/AIS-Logo-1-loading-icon.png00AIS-Hhttps://aisresources.com/wp-content/uploads/2016/11/AIS-Logo-1-loading-icon.pngAIS-H2018-07-30 11:26:052018-08-13 11:51:24MGX Minerals Announces TDEM Geophysical Survey at AIS Resources’ Salinitas Lithium Project, Salinas Grande Salar Argentina

Vancouver, British Columbia – July 25, 2018 – A.I.S. Resources Limited (TSX: AIS, OTCQB: AISSF) (the “Company” or “AIS”) is pleased to announce that the Company has entered into an option agreement to acquire five lithium brine mining tenements in the Salinas Grandes Salar, Salta province Argentina (“Salitinas” or “the Project”). The 4,308 hectare land package resides in the Puna region of northwest Argentina near the border of Chile, an area renowned for its lithium- and potassium-rich brine resources. The surface elevation of the Salinas Grandes salar is approximately 3,400 metres above sea level.

Figure 1. General Location Map of Argentina’s Puna

Figure 2. Location Map of Concessions in the Salar De Salinas Grandes

Under the terms of the Option Agreement AIS has agreed to incur total expenditures of at least US$1.2 million prior to June 13, 2020. The Company can acquire an undivided 100% in the Project at any time during the Agreement by making payments totaling US$4 million. To secure the Option Agreement, AIS has agreed to pay US$250,000.

AIS has granted to MGX Minerals Inc. (MGX) an Option to acquire an 80% interest in the Project. To secure the Option, MGX has agreed to pay US$250,000 on or before July 31,2018. MGX can acquire an undivided 80% in the Project at any time during the Agreement by making payments totaling US$3.2 million. MGX has also agreed to incur total expenditures of at least US$1.2 million prior to May 31, 2020.

AIS plans in partnership with MGX to conduct a Transient Electromagnetic Method (TEM) geophysical study along with trenching, which will be followed by a drill program along the edge of the salar, to test for shallow, near surface brines and determine locations with anomalous concentrations of lithium.

Martyn Element Chairman of AIS stated. “We look forward to beginning a productive partnership with MGX in Argentina.”

Qualified Person Phillip Thomas, BSc, Geol, MBusM, MAIG, MAIMVA, (CMV), a qualified person as defined under National Instrument 43-101 regulations, has reviewed the technical information that forms the basis of this news release, and has approved the disclosure herein. Mr. Thomas is not independent of the Company as he is an officer and shareholder.

About A.I.S. Resources A.I.S. Resources Ltd. is a TSX-V listed investment issuer, was established in 1967 and is managed by experienced, highly qualified professionals, who have a long track record of success in lithium exploration, production and capital markets. Through their extensive business and scientific networks, they identify and develop early-stage projects worldwide, that have strong potential for growth with the objective of providing significant returns for shareholders. The Company’s current activities are focused exclusively on the exploration and development of lithium brine projects in northern Argentina.

On Behalf of the Board of Directors,

AIS Resources Ltd.

Marc Enright-Morin, President and CEO

ADVISORY: This press release contains forward-looking statements. More particularly, this press release contains statements concerning the anticipated use of the proceeds of the Private Placement. Although the Corporation believes that the expectations reflected in these forward-looking statements are reasonable, undue reliance should not be placed on them because the Corporation can give no assurance that they will prove to be correct. Since forward-looking statements address future events and conditions, by their very nature they involve inherent risks and uncertainties. The intended use of the proceeds of the Private Placement by the Corporation might change if the board of directors of the Corporation determines that it would be in the best interests of the Corporation to deploy the proceeds for some other purpose. The forward-looking statements contained in this press release are made as of the date hereof and the Corporation undertakes no obligations to update publicly or revise any forward-looking statements or information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws. Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

https://aisresources.com/wp-content/uploads/2016/11/AIS-Logo-1-loading-icon.png00AIS-Hhttps://aisresources.com/wp-content/uploads/2016/11/AIS-Logo-1-loading-icon.pngAIS-H2018-07-25 09:00:082018-07-26 01:58:37A.I.S. Resources Acquisition of Salinitas Lithium Brine Project at Salinas Grande Salar, Argentina

Vancouver, British Columbia – July 13, 2018 – A.I.S. Resources Limited (TSX: AIS, OTCQB: AISSF) (the “Company” or “AIS”) is pleased to advise shareholders that the UGAMP meeting of the Provincial Mining Environmental Management Unit was convened on July 5, 2018 to review the Company’s exploration plans for the Guayatayoc project. The meeting went very well with no objections to AIS’s exploration activities being raised. A 30-day consultation period is now in effect, during which time further information may be re-quested by the three communities affected. One of the communities Quebraleña, has already signed an assembly document regarding AIS’s planned exploration work program. Marc Morin CEO stated. “The Secretary for the Department of Mines along with his officers were very supportive of our project. He asked AIS to follow up with his department in the next 10 days to get an update on the status of the issue of the drilling permit.” AIS has a drilling company on standby in anticipation of receipt of its drilling permit. The Com-pany intends to complete its seismic analysis, drill six holes to a depth of 350 meters each to test targets at its Guayatayoc concessions. Initially roads will be constructed, then drill pads and four 10,000 litre water tanks.

About Guayatayoc Property AIS has an option over 5,225 ha in the Guayatayoc Salar which hosts favourable geology for lith-ium and was previously mined for boron, which is closely associated with lithium deposition. The salar is adjacent to the Salinas Grades salar and is situated 46km from the main sealed highway. The Company’s January 2017 sampling program sampled two trenches where values of 920 ppm and 270 ppm of Li with Mg to Li Ratios of 1:1 (Refer to February 1, 2017 News Re-lease) were discovered. Thirty five pits were also sampled with encouraging results (refer to February 22, 2017 News Release). Magnesium to lithium ratios were less than 4 to 1, which is excellent for low cost processing. The Company has produced 22 kilograms of samples to date. The AIS team met with Dr. R L Steinmetz PhD and representatives from the National Scientific and Technical Research Council (CONICET) who was able to provide valuable seismic, stratigra-phy and other geological evidence to support the Company’s exploration program. Dr. Steinmetz published her PhD thesis on the Guayatayoc basin in 2013 (Refer to the Company’s 43-101 report for details). AIS may purchase 100% of the Guayatayoc Property by paying $4.5million USD by October 11, 2018.

Representatives of the following groups attended the UGAMP meeting:

Secretaria de Gestión Ambiental.

Secretary of Environmental Management

Secretaria de Derechos Humanos.

Secretary of Human Rights.

Secretaria de Salud Pública.

Secretary of Public Health.

Dirección Provincial de Políticas Ambientales y Recursos Naturales.

Provincial Directorate of Environmental Policies and Natural Resources.

Dirección de Control Agropecuario.

Directorate of Agricultural Control.

Dirección de Industria y Comercio.

Directorate of Industry and Commerce.

Dirección de Recursos Hídricos.

Directorate of Water Resources

Universidad Nacional de Jujuy (UNJU)

National University of Jujuy (UNJU)

Centro de Geólogos.

Geologists Center

Asociacion Obrera Minera Argentina (AOMA).

Argentina Mining Workers Association (AOMA).

Empresarios Mineros (Camara Minera).

Mining Businessmen

Comunidades Indígenas de la zona Proyecto Minero (Quebraleña, San Miguel de Las Colorados and Rincondillas).

Indigenous Communities of the Mining Project zone (Quebraleña, San Miguel de Las Colorados and Rincondillas).

Autoridades Municipales de la zona del Proyecto Minero.

Municipal Authorities of the Mining Project area

Departamento de Control y Policía Minera quien tendrá a su cargo la coordinación de la UGAMP.

Department of Control and Mining Police who will be in charge of the coordination of the UGAMP.

Unidad de Gestión Quebrada de Humahuaca.

Quebrada de Humahuaca Management Unit.

Qualified Person Phillip Thomas, BSc, Geol, MBusM, MAIG, MAIMVA, (CMV), a qualified person as defined under National Instrument 43-101 regulations, has reviewed the technical information that forms the basis of this news release, and has approved the disclosure herein. Mr. Thomas is not inde-pendent of the Company as he is an officer and shareholder.

About A.I.S. Resources A.I.S. Resources Ltd. is a TSX-V listed investment issuer, was established in 1967 and is managed by experienced, highly qualified professionals, who have a long track record of success in lithi-um exploration, production and capital markets. Through their extensive business and scientific networks, they identify and develop early-stage projects worldwide, that have strong potential for growth with the objective of providing significant returns for shareholders. The Company’s current activities are focused exclusively on the exploration and development of lithium brine projects in northern Argentina.

On Behalf of the Board of Directors,

AIS Resources Ltd.

Marc Enright-Morin, President and CEO

ADVISORY: This press release contains forward-looking statements. More particularly, this press release contains statements concerning the anticipated use of the proceeds of the Private Placement. Although the Corporation believes that the expectations reflected in these forward-looking statements are reasonable, undue reliance should not be placed on them because the Corporation can give no assurance that they will prove to be correct. Since forward-looking statements address future events and conditions, by their very nature they involve inherent risks and uncertainties. The intended use of the proceeds of the Private Placement by the Corporation might change if the board of directors of the Corporation determines that it would be in the best interests of the Corporation to deploy the proceeds for some other purpose. The forward-looking statements contained in this press release are made as of the date hereof and the Corporation undertakes no obligations to update publicly or revise any forward-looking statements or information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws. Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

https://aisresources.com/wp-content/uploads/2016/11/AIS-Logo-1-loading-icon.png00AIS-Hhttps://aisresources.com/wp-content/uploads/2016/11/AIS-Logo-1-loading-icon.pngAIS-H2018-07-14 13:25:352018-07-14 13:26:29A.I.S. Resources Announces a Successful UGAMP Meeting

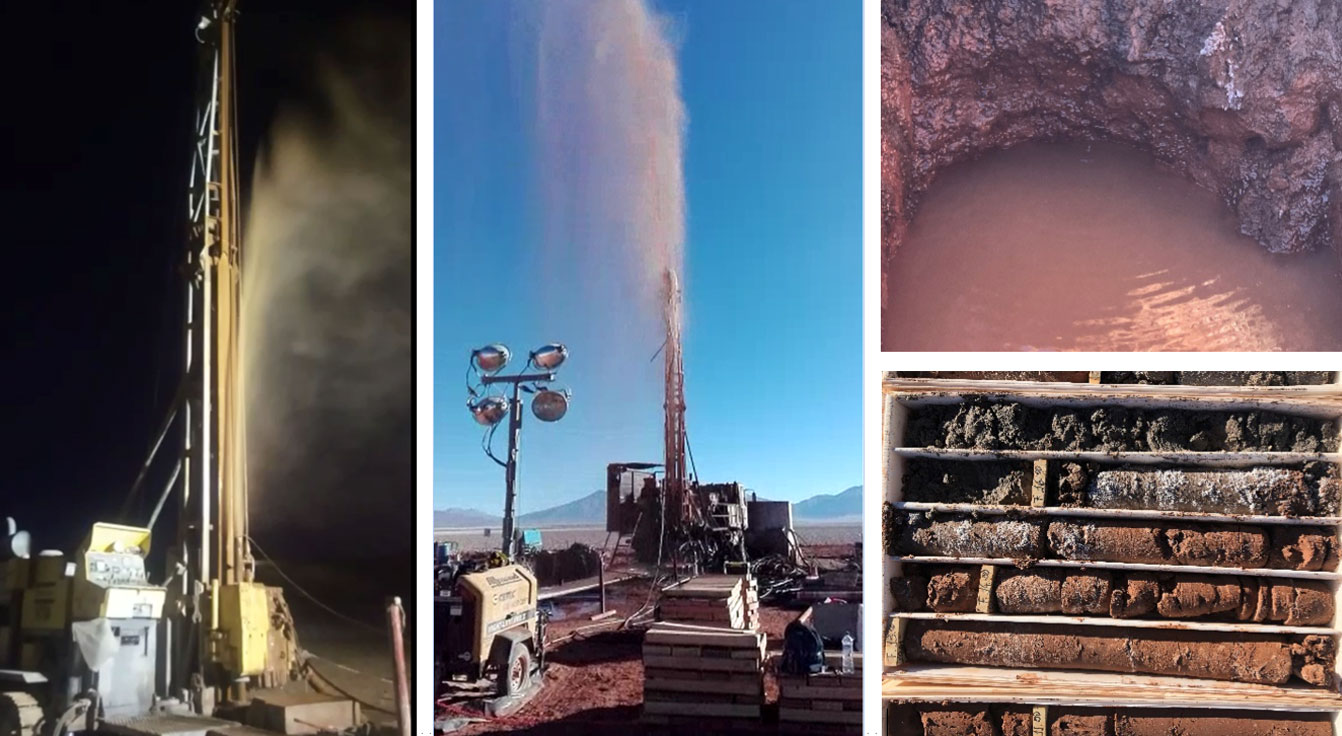

Vancouver, British Columbia – June 12, 2018 – A.I.S. Resources Limited (TSX: AIS, OTCQB: AISSF) (the “Company” or “AIS”) announces it has completed two -90 degrees dip HQ diameter, diamond drill holes for a total of 757 metres, and 21 trenches with depths of 4-4.5 metres in its Pocitos concessions at its Chiron project in the eastern area of the Pocitos Salar. Economic cut-off values were set at 250ppm and 8:1 for Mg:Li values. All DDH hole and pit samples failed this test. The exploration team decided not to continue with the drilling program and exploration work. The Company decided not to exercise the property option which was extended by the vendor until receipt of assay results. Our QP, Phillip Thomas supervised the drill program, sampling and analysis.

Lithium was present in the DDH brine samples taken using a double packer system and were analysed by Alex Stewart Laboratories in Jujuy, Argentina. Two core samples have been sent to GeoSystems Analysis Inc in Tucson, Arizona for specific brine yield measurements, porosity and permeability.

Fig 1 – location of trench pits and drill holes in Pocitos One concession.

Our interpretation of the geophysics was accurate with a major aquifer being encountered at 16m within a black sand unit, indicated by a significant drop in resistivity and at depth where a brown clay unit had transitioned into a coarse sandy unit with halite. High resistivity was correlated to solid halite units with almost no porosity. Significant brine flows at very high pressures were encountered at depth in both diamond drill holes with estimated flow rates of 50,000-70,000 litres per minute. In the case of DDH PO2, the brine flowed under its own pressure for approximately 5.25- 5.5 hours.

Fig 2 Brine from DDH PO1 • Fig 3 Brine from DDDH 2

Fig 4 Pit with brine (upper right corner) • Fig 5 DDH Core showing Black sand unit at 16M (lower right corner)

The results of the double packer (closed downhole sampling) DDH and pit tests are as follows:

Pocitos One – DDH Hole 1

All Values in ppm (parts per million) 100,000 ppm=10% , -90 degrees dip.

Latitude 24˚ 28’ 40.34”S • Longitude 67˚ 01’ 25.01”W

Sample No

Density

Li

Ca

Mg

B

Na

K

Sr Strontium

Mg:Li Ratio

Accuracy

Mg/L ICP

0.05

0.025

0.05

0.05

0.1

0.2

0.01

PO1

1.211

66

788

1111

89

116571

2375

18.17

16.8:1

PO2

40

1197

22

740

116957

1816

27.37

0.55:1

PO3

59

1010

1237

47

113729

2139

23.41

21.0:1

PO4

66

660

1006

105

117887

2475

16.02

15.2:1

PO5

76

588

1100

131

116127

2630

13.05

14.5:1

PO6

1.213

88

581

1258

145

116147

2846

11.73

14.3:1

Pocitos One – DDH Hole 2

All Values in ppm (parts per million) 100,000 ppm=10%, -90 degrees dip.

Latitude 24˚ 28’ 38.59”S • Longitude 67˚ 01’ 00.82”W

Sample No

Li

Ca

Mg

B

Na

K

Sr Strontium

Mg:Li Ratio

Accuracy

Mg/L ICP

0.05

0.025

0.05

0.05

0.1

0.2

0.01

PO2-1

39

1229

758

25

115894

1866

27.12

19.4:1

PO2-2

74

1140

1547

62

106605

1600

23.62

20.9

PO2-3

112

1133

2144

88

103995

1568

20.88

19.1:1

PO2-4

126

1067

2521

111

94408

1392

19.23

20.0:1

PO2-5

95

601

1447

123

116064

2468

12.88

15.23

Pits All Values in ppm (parts per million) 10,000 ppm=1%.

Depth 4.0m-4.5m

Pit No

Li

Ca

Mg

B

Na

K

Sr

Mg:Li

1

22

692

313

31

55,784

998

13.94

15:1

2

No brine

3

65

307

322

209

121722

3201

5.58

4.95

4

No brine

5

45

267

349

53

119763

1623

5.90

7.75

6

No brine

7

72

494

1131

141

116172

2467

9.79

15.7:1

8

76

484

1170

131

118995

2646

10.06

15.4:1

9

78

572

1207

132

116594

2469

10.08

15.5:1

10

179

310

482

316

116856

6375

10.01

2.69

11

80

179

538

1251

116746

2558

10.03

6.72

Pocitos 7 Pits (All Values in ppm (parts per million) 10,000 ppm=1%)

Lat 24˚ 34’ 11.57”S • Long 67˚ 00’ 50” (Pit 12)

Pit No

Li

Ca

Mg

B

Na

K

Sr

Mg:Li

12

72

497

1183

168

118450

2514

9.56

16.4:1

13

72

473

1156

163

115698

2460

8.89

16.0:1

14

73

467

1178

159

121693

2457

8.97

16.1:1

15

65

453

1011

112

121450

2305

8.75

15.6:1

16

68

468

1088

139

119398

2413

8.85

16.0:1

Pocitos 9 Pits (All Values in ppm (parts per million) 10,000 ppm=1%)

Lat 24˚ 35’ 52.86” • Long 66˚ 59’ 20.62” (pit 17)

Pit No

Li

Ca

Mg

B

Na

K

Sr

Mg:Li

17

75

461

1158

148

119869

2587

8.93

15.4:1

18

71

468

1097

126

121774

2612

9.47

15.5:1

19

107

407

1508

143

118643

3629

8.17

14.1:1

20

113

391

1565

143

120195

3815

17.26

13.8:1

21

73

733

480

64

35020

1608

19.53

6.6:1

Interpretation

Both drill holes intersected substantial localized aquifers, however sampling downhole using a double packer tool at 50 metre intervals showed that the lithium values were uneconomic and also the magnesium values were extremely high. Economic cut-off values were set at 250ppm and 8:1 for Mg:Li values.

The geohydrological work on the surface showed that the lithium values in some of the pits with low Na values increased substantially in Lithium and Sodium values over a 7 day period suggesting that surface water drained through the shallow brown sandy clay and black sand unit that had higher porosity due to the sand content, and more lithium rich brines flowed in that had been trapped in the higher density lower clay units. The brine density differential wasn’t measured but the low Na and Li values suggest these surface brines were lower density.

Pit 16 and 19

Was sampled within 12 hours of being dug and then again in 7 days.

Pit No

Li

Ca

Mg

B

Na

K

Sr

16

1

801

41

3

1806

71

4.71

16 -7 days

71

468

1097

126

121774

2612

9.47

19

1

655

84

17

3861

89

7.55

19 – 7 days

107

407

1508

143

118643

3629

8.17

The black sand unit that occurred about three metres below the surface predominately in the central salar area showed substantial porosity and transmissitivity. In DDH 1, 10 metres of black sand core was lost from the drill rod below the 16 metre interval confirming substantial brine presence, but it was low in lithium concentration. The Pocitos Salar was subjected to substantial rainfalls during December to March 2018 and this impacted surface brine concentration. The highest lithium pit value was 179ppm in Pit 10 on the eastern most edge of Pocitos 2. No evaporation studies were undertaken but anecdotal evidence suggests that 3-5cm of water had evaporated over the 30 day drill period.

The geological model adapted from the geophysics survey suggests that brine concentrates to the eastern edge but is stratified by less porous halite and clay units. A cemented aggregate sand sequence was intersected above the brine aquifer at 320-325m in DDH1. Other explorers have confirmed this model in that brines sampled in the west had little or no lithium. We took the view that considering the lithology, deeper drilling had a low probability of intersecting higher lithium grades.

Fig 6 Black Sand unit • Fig 7 Black sand transitioning to Halite Unit

Quality Control and Assurance Alex Stewart International Argentina SA completed the sample analysis using an ICP diagnostic machine. Three samples were submitted in a group of six, and every 10 in 20 for quality control. The variance was 2.5% or less in the lithium analysis, which reflected the variance in brine sampling. ICP machine variance accuracy was 0.05%.

Pit and DDH Packer Sampling Quality Control Each bottle was rinsed in brine. A sampling tool was used to ensure that minimum disturbance was created and the clay sediments were not disturbed. A sample was taken and the cap put on the 1 litre bottles with no air present. The temperature was taken and recorded that was approximately 6.5˚C. The bootle was labelled PO1 or PO2 and then sealed with tape. The QP checked the labelling and recorded it and the site geologist took all the samples to Alex Stewart Laboratories. They sent a confirmation of the date, time and labels of the samples that were received and that they were still sealed.

Guayatayoc Update The company has received the date for its UGAMP (La Unidad de Gestión Ambiental Minera Provincial) meeting slated for July 2nd, 2018. The proposed meeting is for the ratification of our proposed drilling and exploration program at Guayatayoc. The process involves community consultation with government and representatives of AIS.

Once the meeting is complete, a 30 day period for consultation is required, during which time AIS may be requested to provide further information of its planned work program. If no objections are made, the permit will be issued.

Qualified Person Phillip Thomas, BSc Geol, MBusM, MAIG, MAIMVA, (CMV), a Qualified Person as defined under NI-43-101 regulations, has reviewed the technical information that forms the basis of this news release, and has approved the disclosure herein. Mr. Thomas is not independent of the Company as he is an officer and shareholder.

About A.I.S. Resources A.I.S. Resources Ltd. is a TSX-V listed investment issuer, was established in 1967 and is managed by experienced, highly qualified professionals, who have a long track record of success in lithium exploration, production and capital markets. Through their extensive business and scientific networks, they identify and develop early-stage projects worldwide, that have strong potential for growth with the objective of providing significant returns for shareholders. The Company’s current activities are focused exclusively on the exploration and development of lithium brine projects in northern Argentina.

On Behalf of the Board of Directors,

AIS Resources Ltd.

Marc Enright-Morin, President and CEO

ADVISORY: This press release contains forward-looking statements. More particularly, this press release contains statements concerning the anticipated use of the proceeds of the Private Placement. Although the Corporation believes that the expectations reflected in these forward-looking statements are reasonable, undue reliance should not be placed on them because the Corporation can give no assurance that they will prove to be correct. Since forward-looking statements address future events and conditions, by their very nature they involve inherent risks and uncertainties. The intended use of the proceeds of the Private Placement by the Corporation might change if the board of directors of the Corporation determines that it would be in the best interests of the Corporation to deploy the proceeds for some other purpose. The forward-looking statements contained in this press release are made as of the date hereof and the Corporation undertakes no obligations to update publicly or revise any forward-looking statements or information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws. Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

South America’s Prospective by Ellsworth Dickson, Published by Resource Worldon May 11, 2018

With the impending advent of the widespread use of electric cars, trucks plus the millions of rechargeable consumer electronic devices that utilize lithium ion batteries, it is no wonder that numerous exploration companies have turned their attention to the vast Lithium Triangle in Argentina, Chile and Bolivia. It has been estimated that South America’s Lithium Triangle hosts about 54% of the world’s lithium resources.

Exploring Argentina Lithium & Energy’s 20,500-hectare Arizaro Project in northwest Argentina. Photo courtesy Argentina Lithium & Energy Corp.

Most of the world’s lithium has been produced by an oligopoly of producers – often referred to as the Big Three – Albermarle Corp. [ALB-NYSE], private Sociedad Quimica y Minera de Chile (SQM), and FMC Corp.

There are two sources of lithium – hardrock (the mineral spodumene) and lithium brines that formed in desert climates where there is a slow inflow of lithium and other metals and salts but no outflow. Gradual evaporation over thousands of years slowly increases lithium grades to an economic level.

A recent report by Global Market Insights, Inc. concluded that the global lithium ion battery market is set to surpass US $60 billion by 2024 with a global market of 534,000 tonnes of lithium carbonate by 2025. Some lithium mining operations are already producing the world’s lightest metal from brines. In partnership with Toyota Tsusho Corp. and JEMSE, Orocobre has built and is now operating the world’s first commercial, brine-based lithium operation constructed in approximately 20 years. During 2016, Argentina’s two working mines produced 11,845 tonnes of lithium carbonate, or approximately 6% of global output. For 2017, output is about 17,500 tonnes.

Map shows Lithium Triangle located in Argentina, Bolivia and Chile.

In Chile, the Salar (Spanish for salt lake) of Atacama, contains about 27% of the world’s lithium reserve base and provides almost 30% of the world’s lithium carbonate supply. Chile is the most advanced country with regards to lithium extraction, followed by Argentina. On the other hand, it is early days for Bolivia. During a recent presentation in Vancouver, Cesar Navarro Miranda, Minister of Mining and metallurgy for Bolivia, told the audience that the mining sector supports 37% of his country’s population. His government is keen to attract foreign exploration and mining companies by offering various incentives as well as political and economic stability.

Argentina, which already produces about 12% of the world’s lithium, is also keen to attract international mineral explorers. At a recent presentation in Vancouver, Ing. Mario Osvaldo Cappello, Undersecretary of Mining Development and Mining Secretariat for the Argentina Ministry of Energy and Mining, said, “Since February 2016, when President Mauricio Macri took power, export taxes on minerals have been eliminated. There’s a unified currency exchange with a streamlined process. The import of equipment for parts and mining are non-taxed and we also have a free flow of currency. In December 2017, Congress enacted two new laws, so all the investments for the construction of a project will have the VAT refund after six months.”

Capello added, “Up to this year, corporate income tax was 35% and there was no rate for dividends. So this year, the corporate income tax rate is 30% and dividends 7% and, as of 2020, that will change to 25% and 13% for dividends when reinvesting in the country.”

Joseph Grosso, a director of Argentina Lithium & Energy, and an officer of Golden Arrow Resources and Blue Sky Uranium, all with projects in Argentina, has been active in the country since 1993. In addition, to being part of a team that made mineral discoveries, he has been a pioneer in developing the Argentine mining industry.

There is a major question that haunts lithium explorers, miners and lithium stock investors. While increasing demand has boosted lithium prices from US $350 to $3,000 per ton in the past five years, there is uncertainty as to how quickly and how much the electric vehicle market will require.

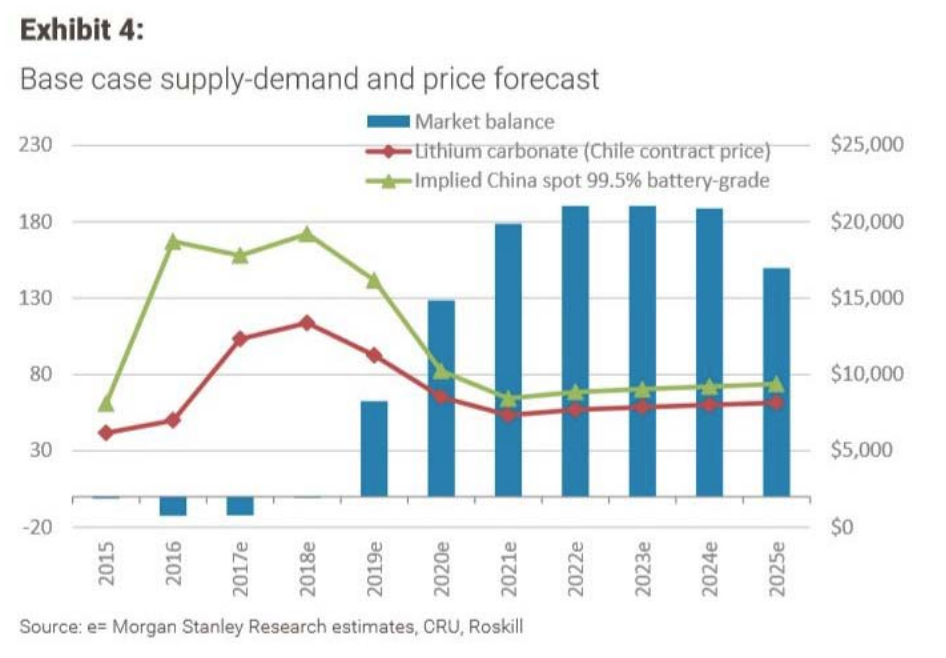

With so many lithium explorers out there seeking economic deposits, plus lithium producers ramping up production, there is no doubt there will be a great deal of lithium supply available. Will that result in an oversupply that will drive lithium prices down? A recent Morgan Stanley report thinks so.

.

On the other hand, major auto manufacturers such as Volvo, Volkswagen and the China’s BYD are betting on mass acceptance of electric vehicles, each with their 30 kilograms of battery lithium, as vehicle prices come down and range anxiety issues are solved. Here is a pertinent question: if the Tesla Semi electric truck is successful, and other sizes of electric trucks are successful too, could this lead to tremendous worldwide sales of trucks? For example, there are some 15.2 million trucks in the US alone with 2 million of them being Semis. Translate that to the rest of the world and the numbers are huge. So what will lithium demand be as well as the demand for the other battery minerals such as cobalt, manganese, copper and graphite?

Below are details on companies active in South American Lithium Triangle.

AIS Resources Ltd. [AIS-TSXV; AISSF-OTCQB]

AIS reported seismic testing has detected three distinct aquifers over a broad area at its Chiron Project in the Pocitos Salar, Salta Province, Argentina. AIS has also completed the mass balance chemistry and process engineering that will be used to determine the raw materials used to purify the lithium brines from its Guayatayoc Project. The data will be used in the design, engineering, and construction of an 810,000 tonne lithium carbonate plant. The analysis used fractional crystallization and ion exchange resins to purify the lithium carbonate to higher than 99.5% lithium carbonate. The work was conducted in Salta and will be replicated at Guayatayoc to ensure that the reduction in air pressure has no material impact.

Advantage Lithium Corp. [AAL-TSXV; AVLIF-OTCQX] has received encouraging assays from its 75% owned Cauchari Project in Jujuy Province, north-west Argentina, about 20 km south of Orocobre’s flagship Olaroz lithium facility. At a brine flow rate of 19 litres/second, there was 515 milligrams/litre lithium and 4,577 milligrams/litre potassium in hole CAU11 in the SE sector.

David Sidoo, President and CEO, said, “This excellent flow rate and lithium grade in hole CAU11 confirms the potential of the SE sector, with the drilling program continuing to provide additional information on the salar geology and brine both laterally and at depth.” The company has 100% interests in five other projects in Argentina.

Alba Minerals Ltd. [AA-TSXV; AXVEF-OTC] is exploring its 2,421 hectare Quiron II property in the Pocitos Salar, Salta Province, Argentina. The company identified a probable lithium brine aquifer at the road accessible Quiron II property through interpretation of a Vertical Electrical Sounding (VES) survey. Alba has an option to earn a 100% interest in the 2,843 hectare Chascha Norte Project in the southeastern part of the Salar de Arizaro, Argentina, the largest yet unknown Salar in this district.

Argentina Lithium & Energy Corp. [LIT-TSXV; PNXLF-OTCQB; OAY1-FSE] has an option to earn a 100% interest in the 20,500 hectare Arizaro Project in northwest Argentina. The road accessible project is near power and rail. Geochemical, electrical surveys and three test holes have been completed. The company has a 100% interest in the Incahuasi Project in Catamarca Province, Argentina with another 10,000 hectares under application. These projects are being prepared for drilling programs.

Dr. Catherine Hickson, P.Geo, COO of Dajin Resources Corp., inspecting a weir box during an active flow test of a well at LSC Lithium’s Pozuelos Project in the Puna region, Salta province, northwest Argentina, where LSC has a NI 43-101 compliant resource of 1.3 million tonnes measured and indicated LCE (Li2CO3) plus an additional 0.5 million tonnes inferred LCE. Photo courtesy Dajin Resources Corp

Dajin Resources Corp. [DJI-TSXV; DJIFF-OTC; A1XF20-FSE] has a strategic partnership with LSC Lithium Corp. in Argentina and has over 93,000 hectares of land holdings. Under the agreement, LSC Lithium has access Enirgi Group’s state-of-the art Direct Xtraction Process (DXP) technology for lithium brines The Enirgi Group has a demonstration plant at Salar del Rincon, Argentina that produces lithium carbonate. Surface sampling on the Salinas Grandes LSC/Dajin JV property of San Jose/Navidad has been completed. Surface pit sampling was conducted as part of the first phase of exploration. High grades were confirmed with concentrations ranging from 281 milligrams per litre (mg/L) to 1,353 mg/L lithium, averaging 591 mg/L. A total of 60% of assays were over 500 mg/L lithium and 8% over 1,000 mg/L.

FMC Corp. [FMC-NYSE] reported that its lithium segment earnings were US $44 million for Q4 2017, up 107% versus Q4 2016. The company produces lithium from the Salar de Hombre Muerto salt flat in northern Argentina.

Galaxy Resources Ltd. [GALXF-OTC; GXY-ASX] is advancing the Sal de Vida (Salt of Life) deposit in northwest Argentina, one of the world’s largest and highest quality undeveloped lithium brine deposits with significant expansion potential. In April 2013, Galaxy released a Definitive Feasibility Study which supports a low cost, long life lithium and potash operation. The study estimated a pre-tax Net Present Value of US $645 million (US $380 million post-tax) at 10% discount rate. Sal de Vida has the potential to generate total annual revenues in the region of US $215 million and operating cash flow before interest and tax of US $118 million per annum at full production rates.

International Lithium Corp. [ILC-TSXV; ILHMF-OTC] and JV partner, Mariana Lithium Co. Ltd., a subsidiary of Jiangxi Ganfeng Lithium Co. Ltd., announced a 2018 budget for continued work at the Mariana lithium brine project in Salta, Argentina. Highlights of the US $17 million budget include continued natural evaporation studies; membrane separation studies; aquifer characterization studies; Preliminary Economic Assessment; and Pre-Feasibility Studies.

Lithium Chile Inc. [LITH-TSXV] has identified a 60+ km2 lithium brine target area at its Helados Project in Chile. The openended, low resistivity zone was discovered by transient electromagnetic surveys within the northwest-trending axis of the Salar Tara Laguna Helada basin. This area displays the same characteristics as the lithium-rich principal aquifers at Salar de Atacama, home to the world’s largest and highest-grade lithium brine mine. The company is preparing for an ini-tial drill program.

LiCo Energy Metals Inc. [LIC-TSXV; WCTXF-OTCQB] is earning a 60% interest in the 160 hectare Purickuta Project and is one of a few “exploitation concessions” granted within the Salar de Atacama, Chile. The property is contained within an existing exploitation concession owned by SQM, and is approximately 3 km north of the exploitation concession of CORFO (the Chilean Economic Development Agency). About 22 km southeast of Purickuta, both SQM and Albemarle have large-scale production facilities within the CORFO concession which collectively produce over 62,000 tonnes of lithium carbonate equivalent annually and accounts for 100% of Chile’s current lithium output.

Lithium Americas Corp. [LAC-TSX, NYSE; LACDF-OTCQX] has a 50/50 JV (Minera Exar) with SQM to develop the Caucharí-Olaroz lithium project in Jujuy, Argentina. The Cauchari-Olaroz pond layout and design have been completed with the pond contractor mobilized at site and production pond construction scheduled to start shortly. Minera Exar has reviewed the development schedule for Cauchari-Olaroz and expects first production to begin in 2020.

Lithium Energi Exploration Inc. [LEXI-TSXV; LXENF-OTC] recently acquired three Argentine corporations, Lithium Energi Argentina, S.A., Antofalla North, S.A., and Antofalla South, S.A., which together hold a portfolio of projects encompassing over 128,000 hectares of lithium brine concessions in Catamarca Province in the heart of the Lithium Triangle, spe-cifically Laguna Caro, Antofalla North and Antofallo South.

Lithium X Energy Corp. has completed a merger with NextView New Energy Lion Hong Kong Ltd. whereby all of the issued and outstanding common shares and warrants of Lithium X were acquired by NextView’s wholly-owned British Columbia subsidiary, NNEL Holding Corp. The company’s 100% owned flagship project is the Sal de Los Angeles lithium brine project, Salta, Argentina. The project comprises about 8,748 hectares of Salar de Diablillos and has a NI 43-101 indicated resource estimate of 1,037,000 tonnes of lithium carbonate equivalent and 1,007,000 tonnes of lithium carbonate equivalent inferred.

LSC Lithium Corp. [LSC-TSXV; LSSCF-OTC] has filed a Technical Report on the Salar de Pozuelos Project, Salta Province, Argentina. The NI 43-101 resource estimate includes 1,296,000 tonnes of lithium carbonate equivalent in the measured and indicated resource category and 497,000 tonnes inferred.

The company has a land package portfolio totaling approximately 300,000 hectares that includes the following projects: Pozuelos, Pastos Grandes, Rio Grande, Salinas Grandes, and Jama. Also, see Dajin.

Millennial Lithium Corp. [ML-TSXV; MLNF-OTCQB; A3N2-FSE] has filed a Preliminary Economic Assessment for the Pastos Grandes Project, Salta Province, Argentina that was prepared by consultants WorleyParsons. The NI 43-101 resource includes 2,131,000 tonnes of lithium carbonate equivalent and 8,141,000 tonnes of potash equivalent in the measured and indicated resource categories, plus 878,000 tonnes of lithium carbonate equivalent and 3,263,000 tonnes potash equivalent inferred.

Neo Lithium Corp. [NLC-TSXV; NTTHF-OTCQX] has discovered a new aquifer at depth at its 3Q Project in Catamarca Province, Argentina. “It adds considerable blue sky to the 3Q Project,” said Waldo Perez, President and CEO. This season, the company focused on completing infill drilling and getting into the deeper part of the basin. The company also reported that processing studies have achieved concentration levels of 3.8% lithium brine solely through solar evaporation – no costly additives were required, plus calcium chloride precipitates through crystallization and in the process captures water molecules within the crystals – both of these represent important developments for the project.

NRG Metals Inc. [NGZ-TSXV; NRGMF-OTCQB; OGPN-FSE] has awarded a contract for the initial diamond drilling at its Hombre Muerto North lithium project in Salta Province, Argentina, to AGV Falcon Drilling SRL. The initial phase of drilling will consist of three core holes up to a maximum depth of 400 metres depending upon results obtained. Drilling is expected to start early April. The project is located at the northern end of the prolific Hombre Muerto salar, adjacent to FMC’s producing Fenix lithium mine and Galaxy Resources’ Sal de Vida development stage project. The Fenix Mine is the largest producing lithium mine in Argentina and the Sal de Vida Project is the largest devel-opment stage lithium project in the country.

Orocobre Ltd. [ORL-TSX; ORE-ASX] is the newest brine based global lithium carbonate supplier through its flagship operation, Salar de Olaroz. Measured and indicated resources are 6.4 Mt LCE capable of sustaining current continuous production for 40-plus years with only ~15% of the defined resource extracted. Orocobre also has a 35% interest in Advantage Lithium.

Ultra Lithium Inc. [ULI-TSXV; ULTXF-OTC] has received assay results of the second round of sampling work carried out in December 2017 on the Salar Laguna Verde discovery zone in Catamarca Province, Argentina. Assay results indicate lithium values in the range of 34.2 to 1,270 milligrams/litre or parts per million (ppm), magnesium values less than 1 ppm to 7,920 ppm, potassium 804 ppm to 15,800 ppm, and boron 65.5 to 2,190 ppm.

Wealth Minerals Ltd. [WML-TSXV; WMLLF-OTCQB; EJZ-FSE] is completing drilling at the Laguna Verde Project, northern Chile. Bench-scale testwork demonstrated Tenova Advanced Technologies’ process technology could be successfully applied to Laguna Verde brines. Wealth signed a JV agreement with stateowned National Mining Company of Chile (Enami) to develop and commercialize Salar de Atacama and Laguna Verde as to Wealth 90%/Enami 10%. Wealth also holds Trinity, Five Salars and other projects in Chile.

https://aisresources.com/wp-content/uploads/2016/11/AIS-Logo-1-loading-icon.png00AIS-Hhttps://aisresources.com/wp-content/uploads/2016/11/AIS-Logo-1-loading-icon.pngAIS-H2018-05-11 12:00:582018-05-23 23:28:23Resource World Provides Update on South America’s Lithium Triangle

While Bolivia has more identified lithium resources than any other country, the current top three producers are Chile, Australia and Argentina. (Image by: Psyberartist | Flickr Commons.)

Economics has been called “the dismal science” for its conclusions which often suggest miserable outcomes for humanity. The saying was born in the 19th century by Scottish writer and philosopher Thomas Carlyle, who was referring to economist Thomas Malthus. Malthus famously calculated that humanity was trapped in a world where population growth would outstrip resources and lead to widespread misery including starvation – a condition known as “The Malthusian dilemma.”

Economics is dismal for another reason: it often fails to make accurate predictions.

We see this in the monthly US employment figures which are usually wrong, and in the copper supply projections trotted out by commodities analysts. Every year these analysts dutifully tally up the predicted market supply tonnage based on output targets from the major producers, and almost every year they turn out to be wrong. Why? Because these so-called experts failed to account for the gaps in output that occur due to strikes, extreme weather, bans on concentrate shipments, or any other reason why a mine closes temporarily due to “force majeure”.

Now the same thing is happening with lithium, with two recent reports coming up with predictions of a slide in lithium prices due to a glut of new supply overwhelmingly the tiny (by mining’s standards) lithium market.

What is puzzling is that both of these reports either gloss over or fail to adequately break down the demand side of the lithium market – something we at Ahead of the Herd did some time ago in a separate article. The conclusion we came to was that lithium demand is skyrocketing, and will continue to do so in coming years, due to the irreversible trend of moving from internal combustion engine-powered vehicles to electric vehicles. The trend is particularly evident in Asia. China is the largest EV market by volume, while Japan is number three behind the US. India is also aggressively ramping up EV targets. Of course we’ve seen the demand scenario play out through lithium prices, which have doubled in the last two years and are current trading at around $23,000 a tonne for battery-grade lithium carbonate. Still, the lithium bears are coming out from hibernation, and lithium stocks have been taking it on the chin. This article will show why they’re wrong.

The lithium bears

In February investment bank Morgan Stanley was first out of the gate with a damning report on lithium; its research team concluded that an avalanche of lithium was in the works and would put the roughly 200,000 tonnes per year lithium market into surplus. The glut would mean a fall to around US$13,000 a ton in 2018, before halving to $7,000 by 2021.

“A host of lithium projects and expansion plans – including increased production by low-cost Chile brine operator SQM – threatens to add 500 kilotonnes per annum to global lithium raw material supply by 2025, swamping forecast demand growth,” Morgan Stanley said.

The main reason for Morgan Stanley’s argument for oversupply was the recent government approval in Chile for mine expansions which would “open up the floodgates” to new lithium product. That is referring to a deal struck in January between Chilean development agency Corfu and SQM, Chile’s largest lithium producer, over lithium royalties in the Salar to Atacama, one of the largest and highest-grade lithium deposits in the world. The deal frees SQM to boost its production quota in exchange for higher royalty rates equivalent to those paid by competitor Albemarle. It also permits SQM to work with state copper miner Codelco to start developing the Maricunga lithium deposit – the second largest lithium-bearing salt brine deposit in Chile. In all the agreement allows SQM to produce up to 216,000 tonnes of lithium carbonate a year from the Salar de Atacama. Lithium supply could also increase due to the election of a new president in Chile, Sebastian Piñera, whose National Renewal Party is open to revisiting a law prohibiting lithium production above 80,000 tonnes.

.

The bank put out a base-case supply-demand and price forecast leading up to 2025, indicating that lithium prices in China and Chile would trend below the market-equilibrium price for the next seven years. Curiously though, the report skewed heavily towards supply with little to no mention of demand.

Morgan Stanley also noted that brine production in Chile has been constrained due to high amounts of magnesium, an impurity in the metallurgical process, but “this is evolving” said the bank, without an explanation how.

Other criticisms levelled at the report: • It makes no mention of the fact that the new royalty rates on SQM are prohibitive and may impede production.

• The report says new production from brines in Chile and Argentina will be low-cost (under $5,000 a ton), suggesting a pulling away of demand from supply. In fact the lithium market is tight, even with new supplies coming online. According to the USGS lithium supply in 2017 was 236,000 tonnes while demand was 228,000 tonnes. Demand forecasts are expected to increase by 2025 according to the

three major producers, Albemarle, SQM and FMC, who will be pressured to produce enough to meet demand.

• The report states that “A bottleneck in conversion capability will keep a lid on realised carbonate production from hard rock mines in the near term – but this is expanding too.” Presumably referring to the

ability of a miner to convert raw lithium into battery-grade lithium carbonate – this statement is never explained, leaving the reader to wonder how hard rock lithium miners are bettering their metallurgy. Lithium is extremely difficult to process from pegmatites and there is currently only one mine doing it – Greenbushes in Australia.

The next lithium bear to wake up was commodities researcher Wood Mackenzie, which forecast a rout in lithium and cobalt – both key ingredients in EV batteries. While Woodmac at least didn’t lowball demand growth – expecting it to grow from 233 kilo-tonnes lithium carbonate equivalent (LCE) in 2017 to 330kt in 2020 and 405kt in 2022 – it too forecast an imminent tsunami of lithium supply. Quoting from the report: … the supply response is under way. Yet it will take some time for this new capacity to materialise as battery-grade chemicals. As such, we expect relatively high price levels to be maintained over 2018. However, for 2019 and beyond, supply will start to outpace demand more aggressively and price levels will decline in turn. – Wood Mackenzie

The London-based firm thus predicts prices will average $13,000 per tonne this year, slip to $9,000 by 2019, and keep dropping to $6,500 in 2022.

Not so easy to make lithium

What the bears seem to have in common is the belief that a rush of new lithium supply will soon hit the market, but what the analysts don’t realize, or maybe for their own reasons neglect to mention, is that a lot of these mines will fail to deliver.

There are two primary means of extracting lithium: from brines in evaporated salt lakes known as salars, and hard rock mining, where the lithium is mined from granite pegmatite orebodies containing spodumene, apatite, lepidolite, tourmaline and amblygonite.

Many junior exploration companies chasing lithium projects are not cognizant of the economic and technical challenges – no brine mining projects and even fewer hard rock projects have been put into production for

the last two decades and when done so it’s been by the major lithium producers in just four countries – Chile, Argentina, China and Australia. This exposes something in the industry no one talks about – a lack of skilled

personnel to get involved with mineralogy/metallurgy and the engineering side of production.

A major factor affecting capital costs for lithium brines is the net evaporation rate – this determines the area of the evaporation ponds necessary to increase the grade of the plant feed. These evaporation ponds can be a major capital cost. Potassium, boron, potash and other minerals are often harvested from early ponds, while later ponds have higher concentrations of lithium. The lithium-pregnant solution is then pumped to an extraction plant

where impurities like boron and magnesium are removed.

Hard rock lithium miners have large problems facing them when competing with brine economics – firstly most have large capital costs for start up and secondly their production cost is roughly twice what it is for the brine exploitation process.

Lithium products derived from brine operations can be used directly in endmarkets, but hard-rock lithium concentrates need to be further refined before they can be used in value-added applications like lithium-ion batteries.

Extracting lithium from spodumene requires a whole range of hydrometallurgical processes. The ore is first crushed and heated in a kiln to create a spodumene concentrate, which is then cooled and milled into a fine powder. It is then mixed with sulfuric acid and roasted again, before waste is separated from the concentrated liquor, and magnesium and calcium are precipitated out. Finally soda ash and lithium carbonate is crystallized, heated, filtered, and dried, creating 99% lithium carbonate. Lithium carbonate is turned into metal in an electrolytic cell using lithium chloride.

Demand “going through the roof”

We’ve been been crunching the supply and demand numbers for almost a decade – at least since President Obama put aside nearly $2 billion in 2009 to support research on hybrid and electric vehicles and their battery components. What we know is this:

Asia and particularly China are looking to lock up lithium supply, and are years ahead of North America in terms of EV penetration and battery supply chains. Last year China sold about 700,000 electric cars, 200,000 more than 2016. Government subsidies to EVs have been reduced by 20%. The Middle Kingdom sees EVs as the key to unlocking the pollution dilemma that has plagued its car-choked cities. China represents over a quarter of the global EV market, and will own 40% by 2040 according to the International Energy Agency (IEA).

The country has signed lithium offtake agreements with mines in Australia, Canada and Africa, and despite Tianqui Lithium – which owns 51% of Talison’s Greenbushes mine in Australia, the largest hard rock lithium mine in the world – being recently denied a 32% ownership stake in SQM, China isn’t giving up. Other Asian companies, such as Japan’s Panasonic and Korean conglomerate Samsung, are also looking to ink deals in the lithium triangle of Chile, Argentina and Bolivia.

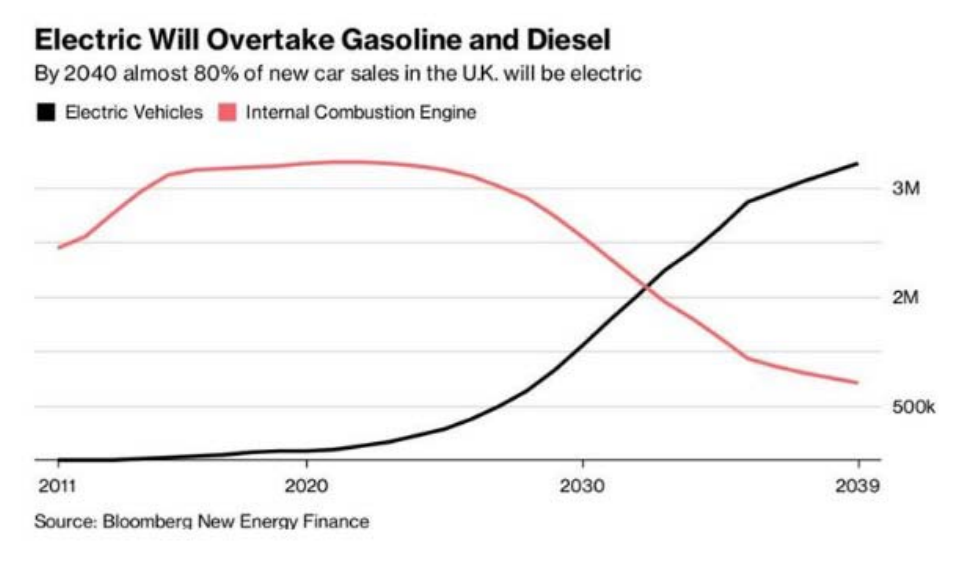

China and India are both going to 100% electric vehicles. Every major car manufacturer has electric models. Volvo has even promised to phase out internal combustion engines (ICE) from 2019.

France has promised to end the sale of gasoline and diesel vehicles by 2040; the UK quickly followed suit. Almost a third of cars sold in Norway in 2016 were electric and Germany could outpace its neighbors as Volkswagen aims to become a leader in both EVs and automated vehicles.

EVs surpassed 2 million units in 2016 and Bloomberg New Energy Finance predicts they will make up an astounding 54% of new car sales by 2040.

.

In 2016, Chinese carmakers sold 28.03 million cars. If China follows through on its promise to go 100% electric that’s a minimum 28.03 million lithiumion battery packs for EV’s per year.

Add in the UK’s 2.7 million car sales in 2016 and France’s 2 million car sales in 2016.

That’s 32.73 million electric vehicles all requiring lithium-ion battery packs, without counting electric buses (a big deal in China, and going to be in India as well) or annual growth rates in auto sales. One Tesla car battery uses 45 kg or 100 pounds of lithium carbonate.

A million electric cars produced in North America means 45,454,000 kg/ 100,000,000 pounds or 45,454 tonnes /50,000 tons of lithium carbonate equivalent (LCE) has to be mined just for Tesla’s North American electric vehicle production – and Tesla has promised to source North American lithium. Elon Musk, Tesla’s CEO, also has plans to build four more Gigafactories other than the one currently being built in Nevada. And it’s not just about the US. China is also building lithium-ion megafactories, and by 2020 these are expected to grow global production capacity by six times.

Think about those global 32,730,000 lithium battery packs.

If each used the same amount of lithium carbonate as Tesla’s electric vehicles, that’s 1.487 billion kilograms/ 3.273 billion pounds or 1,487,727 tonnes /1,636,500 tons of new lithium carbonate demand.

Current annual production of lithium carbonate equivalent (LCE), for all purposes, stands at about 230,000 metric tonnes.

The industry agrees that Morgan Stanley is out to lunch on its forecasts.

“I am firmly of the view that everyone, including Morgan Stanley, is grossly underestimating how quickly the market is moving on the demand side,” Ken Brinsden, chief executive of Australian lithium miner Pilbara Minerals, said at a mining conference in Florida in February.

“Lithium is coming of age in a big way. It’s the core ingredient to 99 percent of electric vehicles and as a result, demand is going through the roof,” Simon Moores, managing director at Benchmark Mineral Intelligence, a UKbased battery metals consultancy, told CNBC.

Another key point is that analysts tend to lump all potential lithium production together, including producers, near-term producers, brines, hard rock mines, and lithium sucked from oilfield brines. The forecasts vastly underestimate the difficulty in extracting lithium from spent oilfields, for example. Some of these wells are up to four kilometers deep, the brine needs to be pumped and trucked to a storage site, then the lithium has to be separated from all the other impurities which could include uranium, thorium, magnesium and potash. It’s neither an easy nor a cheap process and no company has yet been able to do it on a commercial scale.

Canaccord bullish

One consultancy must have had a re-think about the near future of the lithium market. Addressing questions from investors, who likely read the negative reports from Morgan Stanley and Woodmac, Canaccord said in its “Morning Coffee” bulletin that mine production does not necessarily equal LCE supply. In fact mined conversion capacity for 2017 (the amount of lithium actually converted to lithium carbonate or lithium equivalent), 111 kilo-tonnes, was about half their mined LCE estimate of 215kt. Over the next seven years, Canaccord states that more lithium is likely to be mined than can be converted into lithium, thus creating a supply chain bottleneck. This scenario would keep upward pressure on prices. It also expects new lithium to come from higher-cost hard rock mines – likely due to the recently announced expansion at Greenbushes. The mine is set to double in size by next year.

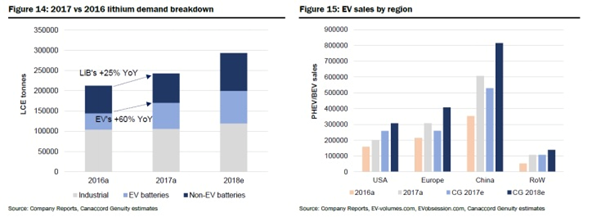

As for demand, Canaccord is bullish, ball-parking 920,000 tonnes of LCE demand by 2025. If that came true, it would be almost five times the current global production. It even admits that figure could be conservative, “with upside risks driven by the increasing potential for demand from LiB-based Energy Storage Systems and larger Electric Vehicle battery sizes (see charts).”

.

.

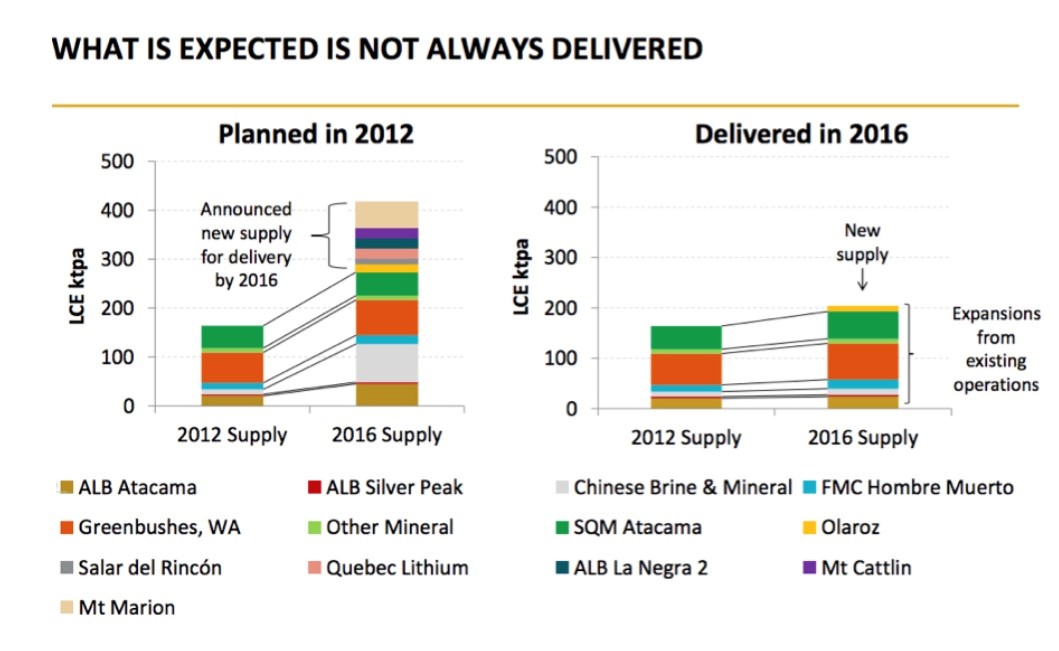

MINING.com riffed on the Canaccord story by noting that both the Morgan Stanley and Canaccord reports referenced a year-old graph from an investor slide presentation from Orocobre, which mines lithium in Argentina. Take a look at the left part of the slide showing that in 2012, major lithium mines planned to produce an extra 200,000 tonnes of new supply by 2016. But when 2016 rolled around, under 50,000 new tonnes came online, despite “expansions from existing operations” (see right part of the slide).

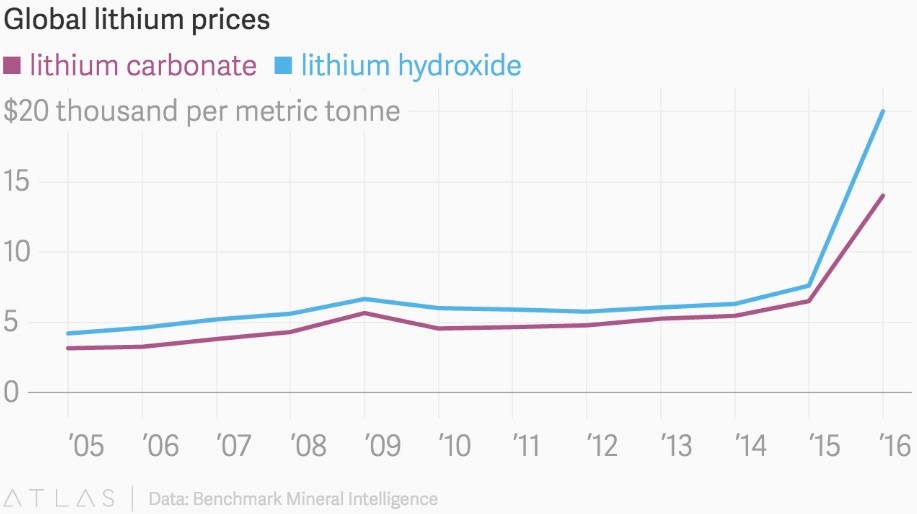

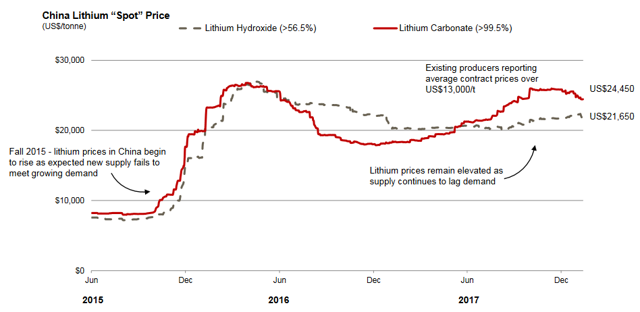

This slide is fascinating for a couple of reasons. One, it proves, like the title, that “What is Expected is Not Always Delivered.” In other words, the major lithium miners despite their best efforts to double production in four years, were unable to do so. Why not? It can’t have been due to prices, which, as seen in the chart below, started heading higher in 2015. As far as we know there weren’t any government policies restricting demand in the producer countries during this period so the only explanation must have been technical challenges in getting the lithium to market.

.

The second reason we love this chart is because it shows definitively how vulnerable the United States is to foreign imports of lithium carbonate especially considering Tesla’s often-stated goal that it plans to source the lithium for its EV batteries from North American mines. The country currently imports most of the lithium that it consumes – with import reliance today pegged at greater than 70%.

On the left of the chart notice the red square denoting Albemarle’s Silver Peak mine – the only producing lithium mine in the United States. We know that Silver Peak has the capacity to produce 6,000 tonnes of LCE per year. They delivered it in 2012 but what happened in 2016? The mine is missing from the right side of the chart, meaning that Silver Peak, located about 200 miles from Tesla’s Gigafactory, failed to produce any new supply to the market. Why not?

If Silver Peak can’t deliver any additional lithium in four years, how can it possibly be expected to supply Tesla’s lithium needs, which as we calculated above, would be 50,000 tonnes of LCE by 2020 if a million Teslas come out of its factory? Let alone four more gigafactories and lithium needed for electric batteries in the Chevy Bolt – the second-best selling EV in the US last year behind Tesla. EV sales in the US, by the way, were up 25% last year compared to 2016, making it the best year ever – giving more ammo to the demand argument.

According to Benchmark Intelligence, Tesla’s Gigafactory also needs about 24,000 tonnes of lithium hydroxide annually, out of a global market of around 50,000 tonnes. Like lithium carbonate, lithium hydroxide is a key raw material for EV battery cathodes.

Given the dearth of current US production, Tesla is looking to Chile to source its lithium, and is reportedly in talks with SQM about possibly building a processing plant. The reason is simple. North American lithium mines are currently too small, not far enough developed, and do not produce a unified product that can easily feed into a supply stream. Tesla would have to go to dozens of different mines for its lithium carbonate and lithium hydroxide. Such a fragmented supply line just isn’t practical.

Lithium in the US

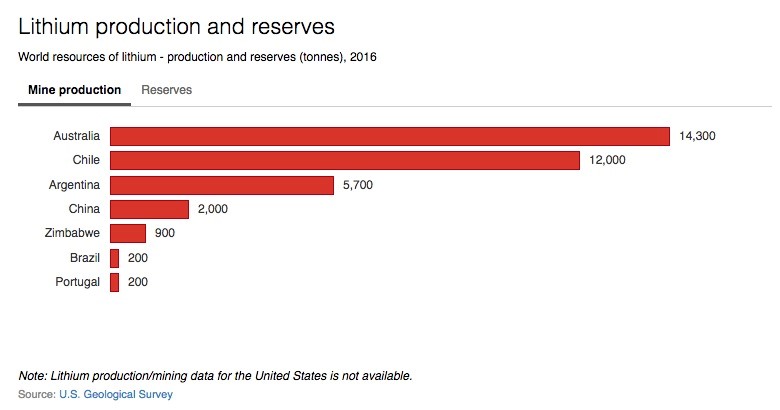

If we want a lithium-ion battery industry and electric vehicles built in North America we need lithium security of supply. No longer can we rely on the good graces of other countries, namely Australia, China, Chile and Argentina, where 90% of the lithium is produced.

We need to develop an energy metals industry in North America – from mine to battery.

Lithium stocks – the producers and the near-term producers – are expensive. There are few bargains to be found among the more developed plays. Fortunately, for investors and our planet’s health, the move towards electrifying the global transportation system is fully underway and appears unstoppable.

And that means earlier-stage, lithium-focused resource plays are going to receive major investor attention.

The old adage, to find a mine, look around a mine, applies here. As mentioned Albemarle’s Silver Peak mine is the only producing lithium mine in the US, but there are other properties around Silver Peak that could become the next big producer and be the solution Tesla has been looking for.

Currently Tesla has an agreement with Pure Energy Minerals to supply lithium hydroxide. Pure Energy’s lithium brine project is located in Clayton Valley adjacent to the Silver Peak mine. It has an inferred resource of 218,000 tonnes of LCE according to an NI 43-101 report filed in August, 2017.

Pure Energy has calculated in a preliminary economic assessment annual production of 10,300 tonnes lithium hydroxide or 9,100 tonnes lithium carbonate equivalent (LCE). Let’s revisit those Tesla LCE requirements. At a million vehicles a year Tesla needs 45,000 tonnes of LCE, meaning Pure Energy can supply just 20% of that.

Where else could Tesla, and Chevy, and any other North American EV maker, source its lithium from in the US? Tesla reportedly wants to reduce its battery costs by 30% in order to make its vehicles more affordable to the average car consumer, and the same is true for other car companies. Getting lithium from the US or Canada, rather than importing it from Australia, South America or China, would reduce shipping costs and provide a ready supply of battery-quality lithium to Tesla and other EV manufacturers. Tesla and Panasonic are making batteries and battery packs at the Tesla Gigafactory, but the lithium produced at Silver Peak is sold to Asian companies, which make cathodes used in lithium-ion batteries. Why not cut out the Asian middlemen and produce everything required for the batteries, right here in North America?

According to the USGS, the United States can only claim about 203,000 tonnes of LCE reserves compared to 75 million tonnes of reserves found throughout the world. That’s about the same amount of lithium currently being produced. But the States has much more lithium than that in the ground. US lithium resources (which include reserves plus lithium that can’t yet be economically mined) currently stand at about 36 million tonnes of LCE, versus 217 million tonnes globally. That leaves a lot of lithium in the US, still to be converted from resources to reserves through exploration drilling.

https://aisresources.com/wp-content/uploads/2016/11/AIS-Logo-1-loading-icon.png00AIS-Hhttps://aisresources.com/wp-content/uploads/2016/11/AIS-Logo-1-loading-icon.pngAIS-H2018-04-29 12:00:212018-05-24 02:21:07Why the Lithium Bears Are Wrong

Vancouver, British Columbia – April 27, 2018 – A.I.S. Resources Limited (TSX: AIS, OTCQB: AISSF) (the “Company” or “AIS”) is pleased to announce it has engaged a second drilling contractor, AGV Falcon S.R.L. of Salta, Argentina to complete up to four diamond drill holes for a total of 1,300 meters across four tenements at its Chiron project in the Pocitos Salar.

AGV Falcon has mobilized a drill rig onto the site and is expected to begin drilling on Saturday 29 April 2018. AIS is looking to expedite exploration at Chiron to gather all the necessary data prior to purchasing the project.

Phil Thomas, Chief Operating Officer and exploration director of A.I.S., stated: “It will be exciting to see the brine results in the core and how well it correlates with the geophysics we have completed. We will drill one hole in Pocitos 2 down to 400m to examine the lithium concentration in the brine at depth. Our modelling suggests there is a significant aquifer at depth but this will give us proof. I will be overseeing the data collection and ensure that QA/QC is monitored and our local geologist will be supervising the packer testing.”

Qualified Person Phillip Thomas, BSc Geol, MBusM, MAIG, MAIMVA, (CMV), a Qualified Person as defined under NI-43-101 regulations, has reviewed the technical information that forms the basis for portions of this news release, and has approved the disclosure herein. Mr. Thomas is not independent of the Company as he is an officer and shareholder.

About A.I.S. Resources A.I.S. Resources Ltd. is a TSX-V listed investment issuer, was established in 1967 and is managed by experienced, highly qualified professionals, who have a long track record of success in lithium exploration, production and capital markets. Through their extensive business and scientific networks, they identify and develop early-stage projects worldwide, that have strong potential for growth with the objective of providing significant returns for shareholders. The Company’s current activities are focused exclusively on the exploration and development of lithium brine projects in northern Argentina.

On Behalf of the Board of Directors,

AIS Resources Ltd.

Marc Enright-Morin, President and CEO

ADVISORY: This press release contains forward-looking statements. More particularly, this press release contains statements concerning the anticipated use of the proceeds of the Private Placement. Although the Corporation believes that the expectations reflected in these forward-looking statements are reasonable, undue reliance should not be placed on them because the Corporation can give no assurance that they will prove to be correct. Since forward-looking statements address future events and conditions, by their very nature they involve inherent risks and uncertainties. The intended use of the proceeds of the Private Placement by the Corporation might change if the board of directors of the Corporation determines that it would be in the best interests of the Corporation to deploy the proceeds for some other purpose. The forward-looking statements contained in this press release are made as of the date hereof and the Corporation undertakes no obligations to update publicly or revise any forward-looking statements or information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws. Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

https://aisresources.com/wp-content/uploads/2016/11/AIS-Logo-1-loading-icon.png00AIS-Hhttps://aisresources.com/wp-content/uploads/2016/11/AIS-Logo-1-loading-icon.pngAIS-H2018-04-27 11:30:102018-04-27 10:31:05A.I.S. Resources Adds Second Drilling Rig at Chiron

LOS ANGELES, April 20, 2018 /PRNewswire/ FN Media Group Presents USA News Group News Commentary

USA News Group – The future of lithium production within South America’s prolific Lithium Triangle is in the balance, as Chile has sent a strong message to China that the nation won’t sell off the majority of its lithium stake. Meanwhile, neighbouring Argentina plays catch up by opening itself up more to the global economy in the aftermath of its own far-left hangover.

The result has been heightened by interest in the activities of companies operating in the Lithium Triangle, including Albemarle (NYSE: ALB), Lithium X Energy Corp. (TSX.V: LIX) (OTC: LIXXF), Orocobre Limited (TSE: ORL) (OTC: OROCF), Sociedad Quimica y Minera de Chile (NYSE: SQM), and A.I.S. Resources Limited (OTC: AISSF) (TSX.V: AIS).

While on its way out the door, the deposed leftist Chilean government left quite a mess for the incoming pro-business elect to deal with-by summoning antitrust authorities to block the possible 32% purchase of Sociedad Quimica y Minera de Chile(SQM) by Tianqi Lithium Corporation out of China. The deal was worth a reported US$4 billion, and once ratified, would leave Tianqi and SQM controlling 70% of the global lithium market.

However, the resistance in Chile has somewhat led to a shift of focus toward neighbour Argentina, which shares dominion over the continent’s renowned Lithium Triangle brine basins. There was considerably less resistance when Lithium X Energyfinalized the sale of its Argentinean interest in an all-cash deal worth $265 million to Chinese investment firm Nextview New Energy Lion Hong Kong Ltd.

Earlier in its development phases, fellow Canadian company A.I.S. Resources Limited has been aggressively moving forward on its four main lithium projects in Argentina’s Puna region, including its preparation for drilling on the potentially lithium-rich aquifers at its Chiron project that were recently detected earlier this year.

With the lingering uncertainty over how Chile will welcome future foreign investments, there’s good reason to believe that companies like Albemarle (NYSE: ALB), Lithium X Energy Corp. (TSX.V: LIX) (OTC: LIXXF), Orocobre Limited (TSE: ORL) (OTC: OROCF), Sociedad Quimica y Minera de Chile (NYSE: SQM), and A.I.S. Resources Limited (OTC: AISSF) (TSX.V: AIS) will be fielding more calls on Argentina properties than the Chilean neighbors.

LEAD-UP TO A LITHIUM STANDOFF

Just days after Chile’s regulatory body in charge of lithium production, Corfo, leveled its recommendation against the Tianqi bid, the Chilean development agency reassured the market by stating that companies from Chine, South Korea, and domestically from within Chile, had been approved to make investments of around $754 million into the country’s lithium industry. However, these approvals would’ve been decided over prior to the March 9th announcement of the Tianqi block attempt.

The Chinese miner Tianqi hasn’t taken this decision lightly, as they have met with Chile’s top anti-trust prosecutor in an effort sort things out. The 32% stake comes from the forced sale on behalf of Canadian fertilizer company Nutrien, which came from the merger of Agrium and Potash Corp. earlier this year.

More Chinese bids are going to come to this region, as the emerging superpower is expected to raise its electric cars production to 7 million units in 2025, up from 1 million last year. Whether deals to secure lithium supplies will all be in the form of the $4 billion deal in Chile, or if it’ll be a smaller deal like the Lithium X deal is still up for grabs.

It’s also likely that Chinese buyers will look to up-and-comers such as A.I.S. Resources to hedge their future supplies, given the junior’s massive footprint across all four of its Argentinean lithium projects. With plenty of blue sky on each project, a partnership or outright acquisition is not out of the question in the future.

THE A.I.S. RESOURCES ACREAGE ADVANTAGE IN ARGENTINA

Boasting four significant lithium projects in Argentina’s Puna region, A.I.S. Resources has secured extremely valuable lithium real estate in the heart of South America’s Lithium Triangle. Located on an elevated plateau that lies east of the Andes Mountains, the Puna Region contains one of Argentina’s largest known lithium deposits.

Spanning approximately 10,457 hectares, A.I.S.‘s four lithium projects are comprised of Chiron 2,732 hectares, Guayatayoc, 2,500 hectares, Guayatayoc III, 2,725 hectares, and Vilama, 2,500 hectares-All of which are surrounded by large, known lithium deposits, operated by prominent lithium majors.

Guayatayoc – the company’s flagship – already has a mining permit, where A.I.S. will soon undergo a TEM-Electromagnetic survey. A drilling permit on the property is expected to be issued before the end of April 2018. The company’s brain trust knows quite a bit about the property already, having already acquired a 2013 PhD study on the property, bringing with it an exploration value worth approximately USD$3 million, and shaving about three years’ worth of work from their timeline.

A.I.S. has compiled a NI 43-101 report on the project, and has completed an environmental impact study. Samples from the Guayatayoc returned Li ranging from 270-900 ppm from brine ponds with aquifer flow, and an added bonus of 100-190ppm brines sitting in the top layers.

The Guayatayoc Salar shares the same tectonic structure that extends to other well-known salars, such as Salinas Grandes, Pozuelos, Pocitos, and Rincón, which hold the most lithium in the Puna Region.

Probably next on the company’s priority list would be the Chiron Project, which consists of four concessions in the Salar de Quirón in the Province of Salta, that other nearby explorers have shown to contain significant prospectivity.

Plenty of drilling is already planned, as evidenced by CEO Marc Enright-Morin’s public statements that A.I.S. is sufficiently funded to drill both the Guatatayoc and Chiron properties in the coming months. With valuable real estate in close proximity to high-market-cap neighbours that include properties held by Orocobre, SQM, and others companies worth more than $200 million, A.I.S. has the project space, upcoming news flow, and milestones ahead to provide plenty of growth potential looking forward.

Hence A.I.S. is a prime example of the type of company that could entice Chinese lithium buyers either for future purchase agreements of product, a development and production partnership, and/or an outright acquisition in the very near future.

Active miners in the industry also includes:

Albemarle (NYSE: ALB) Albemarle Corporation globally develops, manufactures, and markets engineered specialty chemicals. The company offers lithium compounds, including lithium carbonate, lithium hydroxide, lithium chloride, and lithium specialties and reagents for applications in lithium batteries, high performance greases, thermoplastic elastomers for car tires, rubber soles and plastic bottles, catalysts for chemical reactions, organic synthesis processes, life science, pharmaceutical, and other markets; cesium products for the chemical and pharmaceutical industries; and zirconium, barium, and titanium products for pyrotechnical applications. Albemarle Corporation was founded in 1994 and is based in Charlotte, North Carolina.